Fed rate hike - no, Fed doesn't set mortgage nor treasury rates

Fed rate hike - no, Fed doesn't set mortgage nor treasury rates

This is a very common misconception that the Fed sets all rates. The Federal Reserve sets 1 rate-the Fed Funds Rate (FFR).

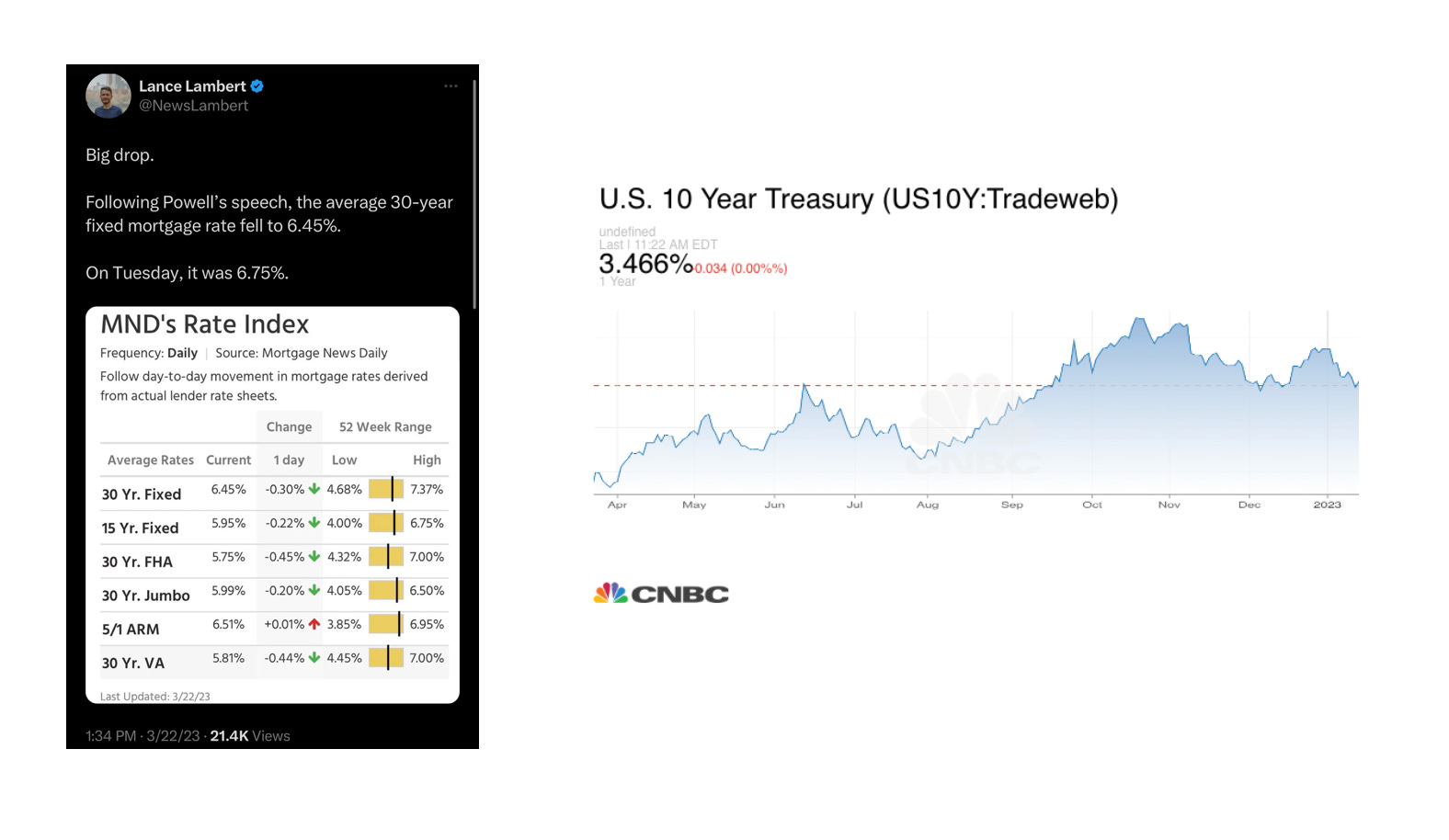

Yesterday the Fed hiked .25 and 30 year mortgage rates fell. Today the US 10Y Treasury yield continues to tick down

In theory when the Fed hikes the FFR which is the shortest end of the yield curve, then one would expect borrowing money for longer periods of time would cost more with higher interest rates. However, this is only true when the yield curve is normal vs it can be inverted. Depending on investors perceptions, on days the Fed hikes the FFR, you may see both the 10Y Treasury & 30 year mortgage rates go higher or lower.

Longer duration Treasury rates are set on the open market. Why do I mention Treasury rates? The 30 year mortgage most closely tracks directionally with the 10 year Tbill. Several mortgage & bond specialists have explained it due to the duration. Most home mortgages duration is 10 years or less due to homeowners either refinancing or selling the home even when they take out 30 year mortgages.

The spread between Treasuries & the 30 year fixed mortgage is a reflection of risk.

What moves interest rates? Ultimately it’s what investors refer to as flight to safety as Treasuries are 100% backed by the US Government and investors outlook. There is an inverse relationship between price & yield. As more people buy Treasuries, the price moves up, and the yield moves down and vice versa. News on jobs/unemployment, inflation, consumer sentiment-debt-spending, global events & instability, politics, war, natural disaster, stock market & other asset class performance all can impact what investors are buying & selling.

The Fed also influences the direction of rates by doing either Quantitative Easing (QE) or Quantitative Tightening (QT). They famously did extensive QE after the Great Financial Crisis by buying not only MBS but US Treasuries & other debt. They had started QT again before Covid hit from 2017-2019, but then reversed course and introduced massive stimulus.

To combat inflation, the Fed is now doing QT by hiking the FFR and has been letting bonds that mature roll off its balance sheet and is no longer buying.

Current conditions reflect high volatility which means rates have been volatile day to day. There have been weeks where rates fell sharply before reversing course and moving sharply north. In other words, do not expect a rate you saw or got quoted yesterday or last week to be relatively the same.

Mortgage rates move constantly, sometimes multiple times throughout the day. The rate you will get for your purchase or refinance is conditional on when you lock the rate.

What does this mean for multi-family? For 5+ units, you can still find favorable rates right now as I had a conversation with a Chase residential commercial banker yesterday. If you are looking for construction loans or anything that is what is referred to as non-vanilla in the banking world, then lending may be more challenging as some regional lenders have paused their commercial lending. Currently the majority of the real estate distress is happening in the commercial world.

If you are considering selling, rates are going to impact the number of Buyers who qualify or who will be cash strapped as they kick in more of their savings & investments to qualify on DTI (debt to income ratio). Some Sellers are currently offering money to pay down a Buyers rate. 2-1 Buy down programs are back!

Call me to discuss the benefits to both you and the Buyer.

For more information on mortgage rates, talk to a mortgage lender and read my Mortgage FAQs 3 part series starting here: