Lock-in effect of mortgage rates & Prop 13

When will we see more listings on the market in San Diego? I don’t think we’ll see dramatic increases in listings until we see widespread distress where homeowners need to sell to access the full equity in their homes or they cannot take out a HELOC.

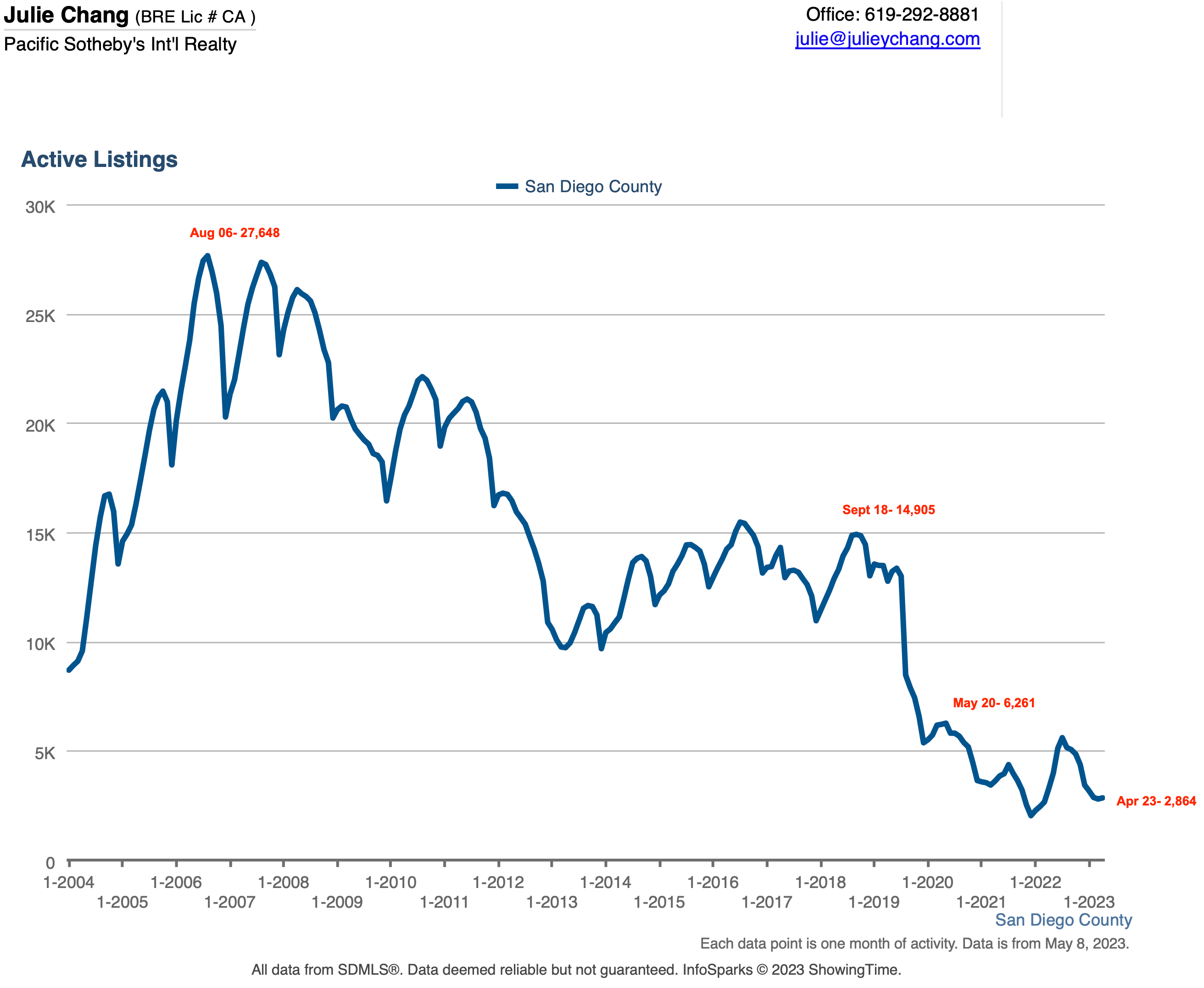

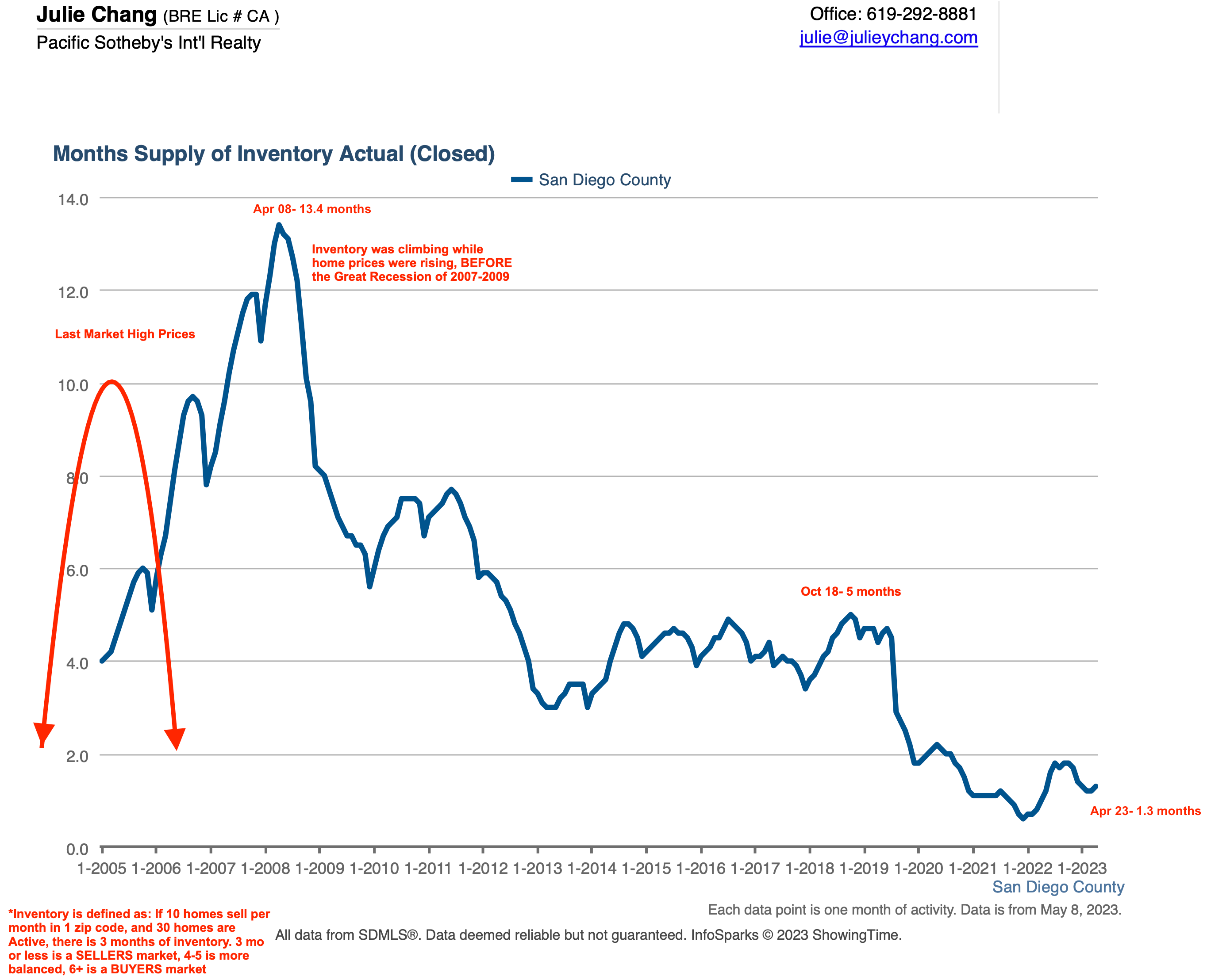

In total listing volume or Active listings, we are way down San Diego Countywide. Inventory = Active listings / number of homes sold per month or Months of Inventory, which reflects supply & demand is also very low. We have been sitting at 1 months of Inventory or lower for many zip codes for some time now.

Yes, across single family detached, condos, townhomes, row-homes, manufactured homes including age restricted 55+ listings, we have less than 3000 total Active listings in the entirety of San Diego County. As of this writing, we have ~2232 Active or Coming Soon listings (Source: SDMLS)

Normal life events that cause people to move include the notable D’s- death, disability, divorce, distress. There is also job relocation, need/want for smaller/larger homes, wanting to change product type (SFR to condo) that add to the usual turnover of homes, moving into senior housing.

With Fed moves from ZIRP to rapid QT & rate hikes to drive rates up, the lock-in effect or the golden handcuffs of the existing cost of housing is limiting owners’ ability to move up or move down. Coupled with Prop 13 property taxes basis in California, and the very low number of homes in any given zip code, within price points, the ability to move is challenged by the reality of math.

This lock-in effect is in residential lending assuming fixed rates. Conversely, the rapid interest rate moves are impacting rates that have adjusted, non QM, 5+ units, commercial & construction debt. Commercial loans are structured very differently with shorter loan maturities, balloon payments, floating rate debt, multiple tranches of debt in their capital structure, loan covenants. Much of what is in the news about distress in real estate is around commercial, which is further nuanced as to what categories of CRE are impacted.

When you layer in homeowners who own their homes free & clear, almost 40%, it is hard to imagine there will be significant foreclosures or panic Sellers in San Diego. Of course in the case of a black swan event, all bets are off. With inventory levels at record lows, we could see 3-5x in months of inventory before it becomes a strong Buyers market

Can I Afford to Move?

For simplification purposes, I’m going to use numbers knowing that every scenario is going to vary and not accounting for utilities, maintenance, etc. For your purposes when evaluating equity / net proceeds on a sale, your numbers will be impacted by:

your purchase price, basis after repairs/upgrades/costs

your stepped up Prop 13 basis

how much equity is in your home depending on if/when you refinanced, whether you pulled equity out

what your capital gains exclusion is + your income tax rate

Original Purchase

You bought a 2 story detached 2800 ESF, 5 bedroom, 3 bath home around $1M ~7-10 years ago

Your current mortgage rate is 2.5% with an 80% LTV or $800,000 loan amount

HOA & Mello Roos = $500 /month

You sell the home for ~$2M

Your net proceeds after taxes, fees, paying off your mortgage = $900,00

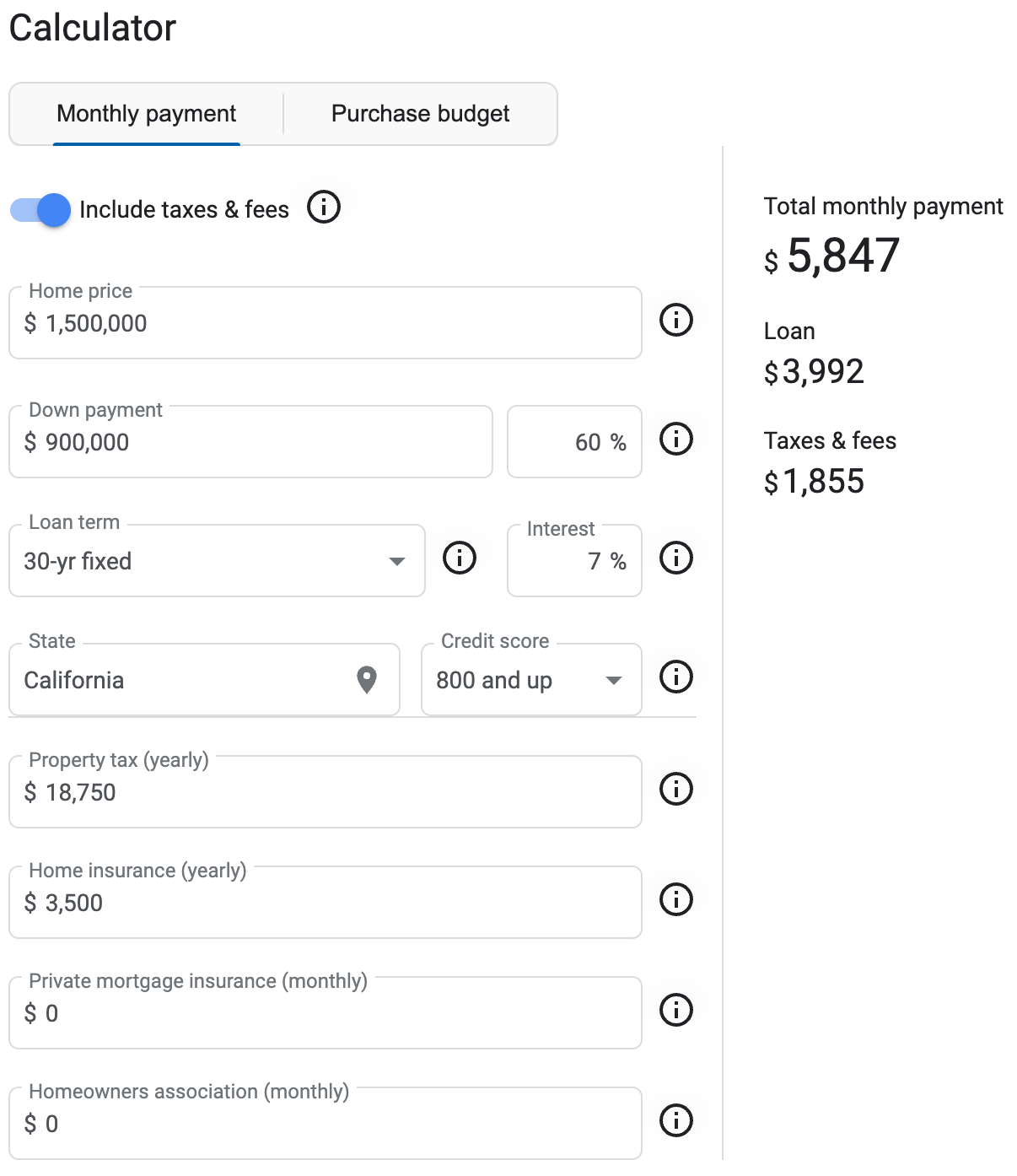

Google Mortgage Calculator

New Purchase

You downsize to a ~$1.5M, 1 story detached 1300 ESF 2 bedroom, 2 bath home

Current mortgage rate is 7%, using all of your sale proceeds to put $900k down for a 40% LTV or $600,000 loan amount

No HOA nor Mello Roos

Your Monthly Payment goes up. Now imagine if you have a $500-$1000 monthly HOA fee if you moved into a condo

New Purchase with Repairs/Updates Needed

If this new home needs work, you put 50% down or $750,000, 50% LTV, instead so that you have the cash to do the repairs/updates

Your monthly payment is now $1,850 higher than if you just stayed in your larger home

Google Mortgage Calculator