Are you prepared to hold through the next cycle?

Are you prepared to hold through the next cycle?

Real estate, like the economy runs in cycle. We have had a really long cycle from 2008-2022. In residential housing, we hit new price highs this year in San Diego from sales of very limited inventory.

If you are thinking about selling RE, the question always is, if you don’t sell today, are you prepared to hold for the next 7-10+ years? Likewise if you are planning to buy RE, be prepared to hold long term. If market conditions become unfavorable to sell without losing money, can you rent it?

A lot of discussion about how RE will fare happens in an isolated perspective assuming everything else is not changing. I hear these narratives frequently: a lot of owners have a lot of equity, RE demand is high, we are not building more fast enough, employment is high.

Nothing is constant- you should not make assumptions that equity will not decline if asset prices fall, the stock market will not experience sustained losses, people will not experience loss or decline in income, or the cost of insurance becomes unaffordable. Past performance does not equal future performance. This time last year the herd was optimistic about real estate and the economy. In recent months, there has been endless negative news. Loss of confidence can become reality if people panic sell.

There are some major headwinds ahead:

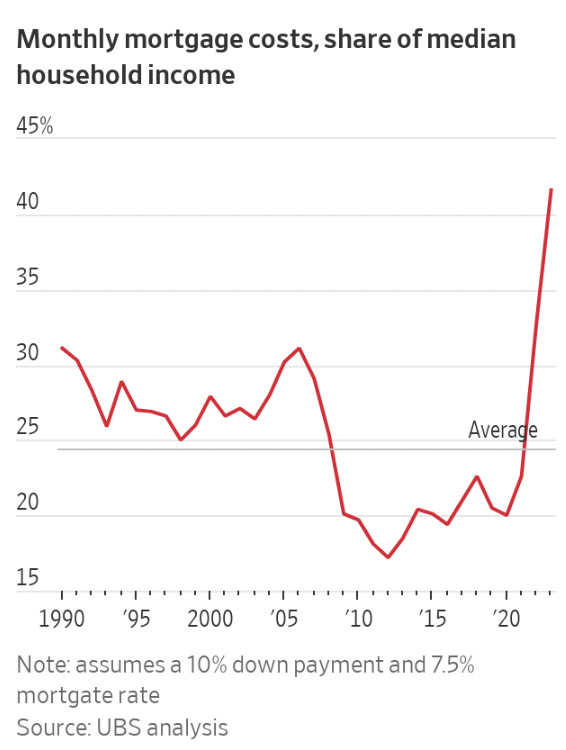

30 year mortgage rates have hit a 22 year high. Mortgage rate surveys are not normalized, meaning 1 lender can quote at .5 points, another with 1 point and so forth so these rates may have a cost to them to get that rate. In San Diego we have both the national conforming loan limit but also a high balance one which impacts the rate. There is no such thing as parity in rates and rates are ever changing based on market conditions.

The pool of qualified Buyers is shrinking. Buyers must qualify on debt to income ratios. In the past several years we’ve seen Buyers using more & more cash to get their loan amounts down to qualify. Buyers have been diligently saving, benefiting from investment gains, gift money from family, but with rates moving rapidly and prices not budging, some Buyers are simply tapped out.

The spread between rent and ownership cost for condos just doesn’t make sense for most Buyers to even consider buying a condo, especially when there are so many units to rent. Townhomes and Detached homes continue to be inventory constrained for both rentals and the features they offer or are desired, such as condition, allowing pets, garages, etc.

Yield Curve: I hear a lot of the RE industry say buy now before interest rates drop and all of the Buyers on the sidelines pile into the market and you’re competing against 20+ offers again. Why are rates dropping?

If the Fed is doing QE again by buying MBS, or cutting the Fed Funds Rate, and investors are buying the 10Y Treasury to push long term yields down (30Y mortgage most closely tracks with the 10Y Treasury), this is a flight to safety move and something is very wrong with the economy.

Right now the yield curve is inverted and people are buying short duration treasuries given the higher yields plus greater liquidity.

Credit card default rates on the rise: “Americans’ Credit Card Debt Tops $1 Trillion, Hitting All Income Levels”

“The average credit card interest rate is 28.06%, according to Forbes Advisor’s weekly credit card rates report”

Student loans: Repayments resumed October 1st. 45% of borrowers expect to be delinquent. For 12 months, this will not affect borrowers credit.

Per the WSJ: “The restart of student-loan payments could divert up to $100 billion from Americans’ pockets over the coming year, leaving consumers squeezed and some of the nation’s largest retailers fearing a spending slowdown.”

If you are a Seller, we should discuss advertising your property offering a Seller paid buy down on the rate. Optics, market psychology, Buyer cash flow will impact interest in your property. Your goal as a Seller is to get the highest & best price with a Buyer that will actually close. This means you want as many Buyers as possible writing offers on your property. If you can get Buyers to compete for your property, this typically means Buyers will drive the price of the home up. Sellers paying for a rate buy down is far more cost effective to both you as a Seller (net proceeds) and the Buyers (monthly payment) than if you did a comparable or larger price reduction

Rental demand nationally is softening: I wrote about seeing a lot of rental units advertised for rent plus new construction coming online. If you are an investor looking to buy income units thinking you can use today’s rents to run pro forma projections, you should also run scenarios with lower rents & higher vacancies. Lenders in underwriting may also be using more conservative numbers, requiring higher DSCR and lower LTV.

Jay Parsons shares: “I wouldn't call it "oversupply" because that implies a structural issue, but a better description might be a "short-term supply/demand imbalance." We're still structurally undersupplied on housing, but it's just incredibly tough to absorb this much supply in such a short period of time -- even with healthy demand drivers in place.”

Insurability & costs: Frequently I’m seeing someone on X tweeting about how much insurance costs are rising or how they got dropped by their insurer. This is happening in many states, including CA. Insurance is going to be a huge factor in RE costs and affordability going further for both homeowners & investors. Condo association master insurance policies are getting dropped by insurance companies and forcing more to seek alternatives or into the CA Fair plan.

When buying property, consider what risks there are for fire, flood, mudslide not only in the short term, but in the years to come. Insurance policies are required if you have a mortgage. Do you know about managed retreat? Some people think buying property on the coast or a block from the ocean means you will be less likely to see major asset value decline but have you considered how government policy & insurability will impact future value?

Do your homework by talking to insurance agents early in the due diligence period.

Opportunities: for those of you who have been diligently saving and waiting patiently, we will have to wait to see how this unfolds for San Diego opportunities. The distress thus far has primarily been in commercial asset classes, including multi family (5+ units) and in other areas of the country that may be less resilient to economic decline. When evaluating opportunity, trying to time the market is difficult. Does the math work? Is this an asset you plan to hold long term? In residential, the decline is not fast. If you remember the GFC, it took from 2006 to roughly 2012 to go from peak to trough and then many more years to get back to prior hights. Not everyone is going to experience distress, some will experience it at different points, but most people will hang onto to their primary home or smaller MF building like their life depends on it as the last assets they give up on.

If you are reading about other real estate investors or homebuyers finding deals, keep in mind that opportunities are not the same in different markets and asset classes. Real Estate value is very specific to the type of real estate and location -it is hyperlocal.

Some investors have built relationships over 20+ years and will have access to opportunities most people will not have. Some investors are not relying on bank debt as they have access to private capital. They may have a fund in which they need to deploy the capital and generate investor returns on a different time horizon than yours.