ADUs, jADUs, multi-family+ bonus density

ADUs, jADUs, multi-family+ bonus density

If you are looking to house hack, buy a single family home to add units, or build more units or ADUs on your property, here are some key areas to do your homework.

If you have no experience, it might be prudent to leverage an expert who has built similar projects and has experience working with the applicable city or county.

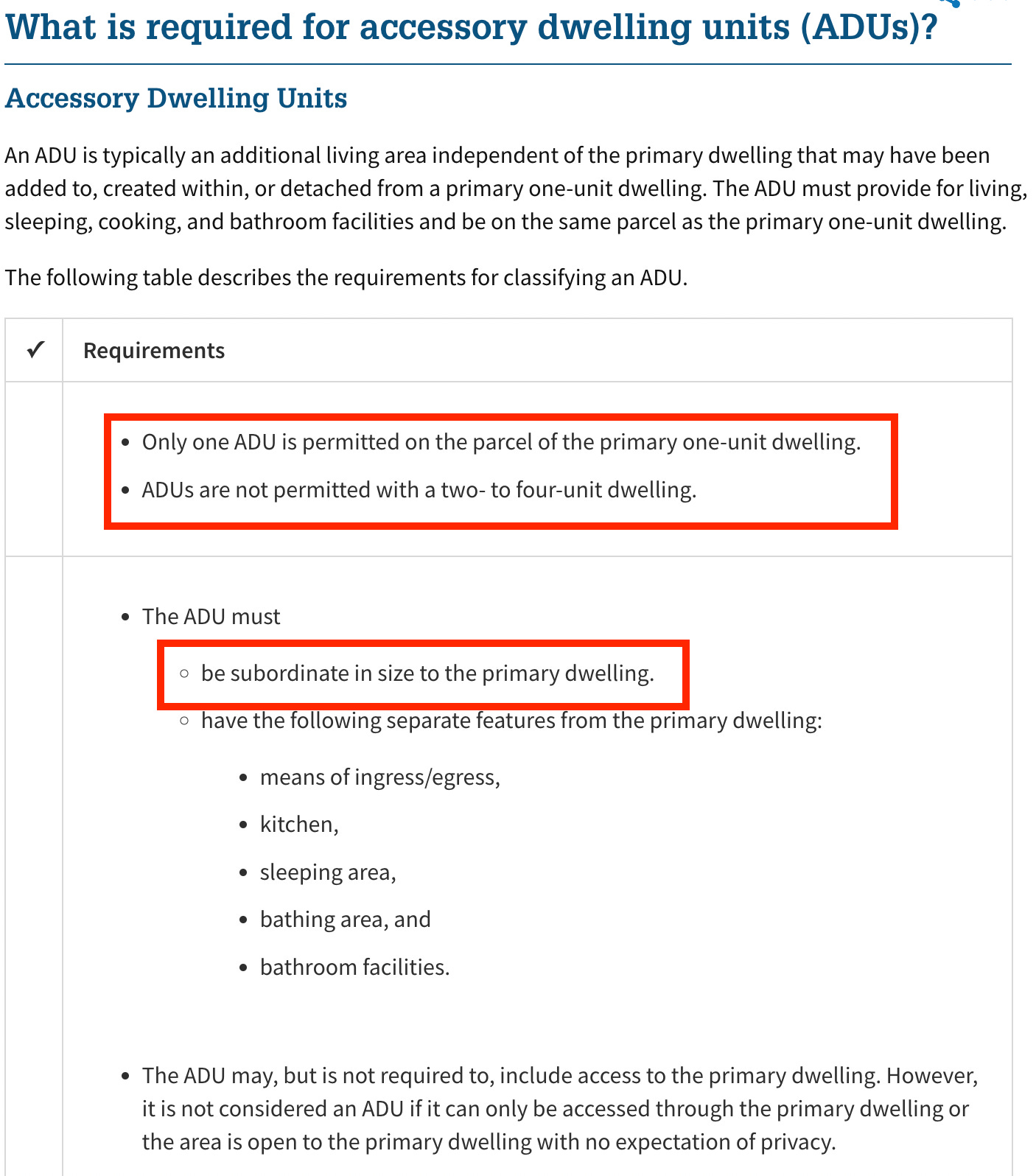

The primary question I get is what is the difference between multi-units vs multi-units + ADU or SFR + ADU. Aren’t they all units? Well yes, but they are different.

The short answer is there are restrictions on use, size, how it’s built, as imposed by the relevant city and also in the lending world. In lending, 4 units or less is residential, 5+ units is commercial. Depending on residential vs commercial lending, ADUs do or don’t count as a unit.

Development / Zoning / ADU guidelines

What jurisdiction applies? Some cities have their own ADU guidelines. The County has ADU guidelines. Some cities follow state guidelines

How is the property zoned? Does it fall in an overlay to allow for more density?

If the property is zoned RM for multi-units, can you build more units per the RM zoning? What overlays restrict/allow for building?

I’ve linked to the City of San Diego zoning, but within the county there are many disparate city governments, so check with the city or San Diego County where applicable

For example, if the property is zoned “RM-2-4, permits a maximum density of 1 dwelling unit for each 1,750 square feet of lot area”, can you build more units under this zoning first? Then can you leverage any overlays, other bonus density to add ADUs?

If the property is zoned SFR in the City of San Diego, does it fall into a Complete Communities or Transit Priority Area overlay?

If you are able to leverage bonus density for ADUs please refer to income restrictions for bonus ADUs. If you want to leverage bonus density that allows for greater units that are not ADUs, please review those development guidelines including affordability

Multi-family units vs ADUs have different rental length restrictions - check with your city/county. Example: ADUs can require 30+ day rentals only

Has the lot been downzoned? If the property has 3 units on it but the lot has been downzoned to SFR, is this a legal non-conforming use as it stands? You will want to check with the jurisdiction on whether you are allowed to add ADUs

If the property has Mills Act or is historical, you will need to check with the jurisdiction on what is allowed to be built

Lending- this is a significant consideration that may determine what you build. I recommend you speak with multiple lenders and guidelines do change.

Multi-units that are permitted 2-4 units fall under residential lending, but have their guidelines that differ from single family or condos. In multi-units, 75% of the income can be used to qualify for the mortgage on units that you don’t intend to inhabit.

For ADUs, if you want to be able to leverage GSE backed financing aka conventional mortgages, you will want to be mindful of Fannie Mae & Freddie Mac guidelines

For the purposes of loan limits, multi-units count towards the higher per unit loan limits but ADUs do not. If you had a SFR with an ADU, this falls under SFR lending loan limits & guidelines.

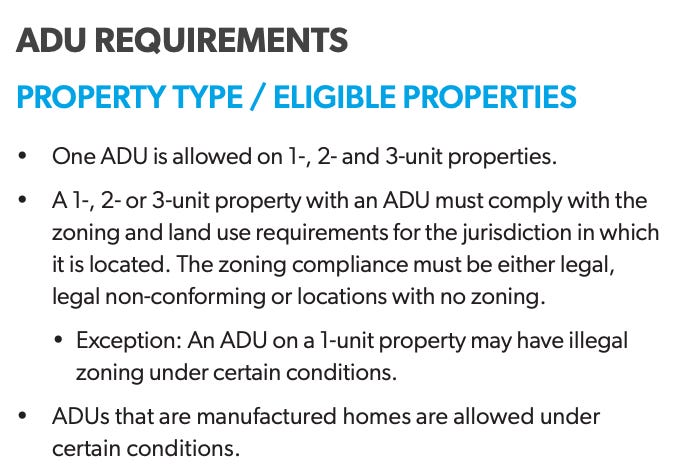

Fannie doesn’t allow more than 1 ADU on a property. Therefore if you have your primary home + 2 ADUs, this is not Fannie lendable

Fannie doesn’t allow any ADUs on 2-4 unit properties

Fannie doesn’t count ADU income

Freddie allows 1 ADU on 1, 2 & 3 unit properties

Freddie does count ADU income

Commercial loans, non QM, portfolio loans

Many commercial lenders will not do loans on properties unless there are 5+ units. However there are lenders that will offer options for under 5 units using commercial loan programs

If you’ve never done a commercial loan, this is a different lending world. Commercial, non QM or portfolio loan world is very lender & program specific with respect to guidelines. You will want to shop across options and dig into the details on all of the loan requirements & restrictions

In general, portfolio loans, non QM loans can be higher in rate, but not always. Some regional retail banks will offer preferred rates to clients with a banking relationship that requires assets to be held at the bank

The property itself matters significantly on what lenders will loan on it

They may be shorter in term, varying amortization, recourse or non recourse, different costs, DSCR requirements, take longer to close, loan covenants that make them call-able

Summary

If you are buying a property hoping to re-develop, I recommend you do copious due diligence including leveraging consultants, developers, and architects with experience on similar projects. As a Realtor, I do not interpret zoning for clients. This is ultimately up to the jurisdiction the property falls as to whether you will be allowed to do or build XYZ.

Before you build additional units, absolutely consider the lending impact. While the GSEs may change their guidelines in the future, your ability to sell the property or refinance can be impacted by what you build.